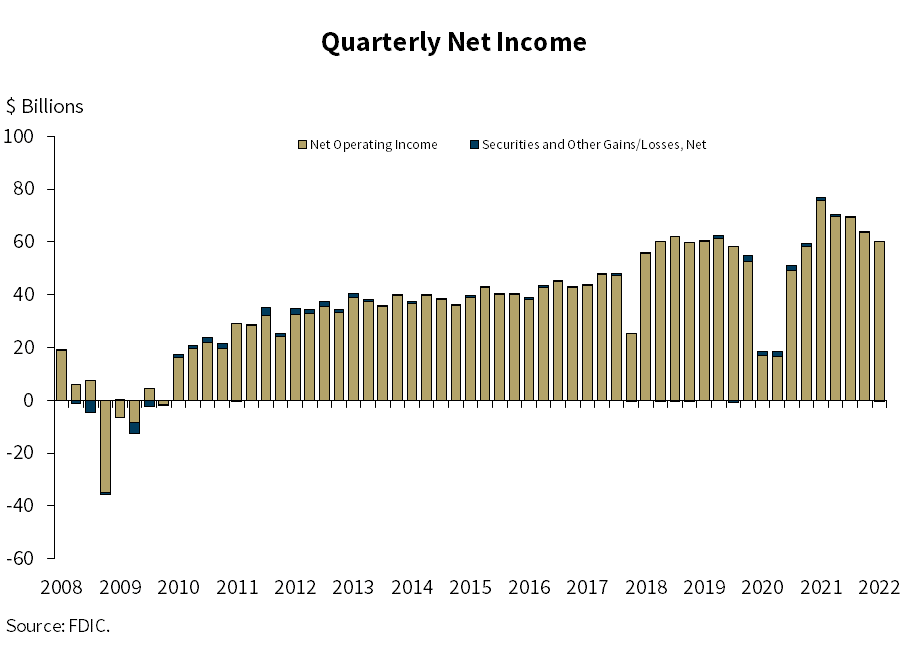

FDIC-insured institutions made $59.7 billion in net income during the first quarter of this year, a 22-percent drop from a year ago, according to the Quarterly Banking Profile.

FDIC-insured institutions made $59.7 billion in net income during the first quarter of this year, a 22-percent drop from a year ago, according to the Quarterly Banking Profile.

The overall drop was due to a $19.7 billion increase in provisional expenses, mainly among the largest banks. Nearly 63 percent of banks reported an annual decline in quarterly net income.

“The increase in provision expense reflects, in part, a slow return to pre-pandemic levels, reflecting an increase in loan balances and evolving economic uncertainties,” said Acting FDIC Chair Martin Gruenberg. “Though the increase in provision expense has reduced income, it has also increased protection against future losses.”

Community banks insured by the FDIC made $1.1 billion or 14 percent less in net income on a year-over-year basis during the first quarter. That was a smaller decline than larger banks experienced, Gruenberg noted, as revenue from loan sales declined and business expenses increased. Smaller banks saw a 1.3 percent increase in loan balances from the previous quarter and 2.1 percent growth from the year-prior, driven by commercial real estate loan growth. “Excluding PPP loans, total loan growth rates for both the industry and community banks would have exceeded pre-pandemic average growth rates,” Gruenberg noted.

Year-over-year net interest income for community banks grew by nearly $793 million as interest income on securities increased $655.5 million or 34.2 percent, and interest expenses fell $630.3 million or approximately 29 percent. Net interest income declined by 1.1 percent, and provision expenses tumbled 31 percent from a year ago and 18.3 percent from Q4 2021. Community banks’ net interest margin narrowed 15 basis points from Q1 2021 to 3.11 percent, as earning asset growth outpaced net income growth. Community banks experienced record lows in both noncurrent and net charge-off rates.

“The FDIC’s latest quarterly report demonstrates that the banking industry remains healthy as it supports the U.S. economy amid rising inflation and headwinds from the Russian invasion of Ukraine,” said Sayee Srinivasan, chief economist of the American Bankers Association. “Credit quality is exceptionally strong and lending continues to gain steam following robust growth in the previous quarter.”

Despite ongoing payment and forgiveness through the Paycheck Protection Program, total loan and lease balances for all FDIC-insured banks increased by 1 percent or $109.9 billion from the previous quarter. Fueled by growth in consumer lending, nonfarm nonresidential CRE loans, and loans to nondepository institutions, year-over-year loan and lease balances increased nearly 5 percent or $531.8 billion from the year-ago quarter. Year-over-year quarterly net operating revenue grew by nearly 4 percent to $214.7 billion.

The loan market remains strong: Loans 90 days or more past due or in nonaccrual fell by 4.5 percent from the previous quarter, and the noncurrent rate for total loans fell 5 basis points to 0.84 percent. Total net-charge offs fell 32 percent from a year ago, and the total net charge-off rate dropped 12 basis points to 0.22 percent, only slightly above the record low set in the third quarter of 2021. Banks reported an aggregate return on average assets ratio of 1 percent, down 38 basis points from Q1 2021 and nine points from the previous quarter. NIM declined by one basis point from the previous quarter to 2.54 percent, but remains four basis points higher than the record low established in the second quarter of 2021. The yield on earning assets decreased to 2.7 percent, down one basis point from a quarter ago and 7 from a year ago, as the growth of average earning assets continued to outpace interest income growth.

The Deposit Insurance Fund balance remained relatively unchanged from the previous quarter at $123 billion. The reserve ratio dropped 4 basis points to 1.23 percent, as insured deposits increased 2.5 percent.

According to the FDIC, 44 institutions merged and no banks failed in the first quarter of this year. The number of problem banks is at its lowest level since the Quarterly Bank Profile data began tracking the number in 1984. Banks also added jobs during the first quarter, Srinivasan noted, with industry employment rising by 19,000.