FDIC-insured institutions made $68.4 billion in the fourth quarter, a 4.6 percent decrease from the previous quarter. That lower number was caused by a drop in noninterest income and a large increase in provision expenses offsetting an increase in net interest income, according to the agency’s Quarterly Banking Profile.

FDIC-insured institutions made $68.4 billion in the fourth quarter, a 4.6 percent decrease from the previous quarter. That lower number was caused by a drop in noninterest income and a large increase in provision expenses offsetting an increase in net interest income, according to the agency’s Quarterly Banking Profile.

Year-over-year net income for the 4,258 FDIC-insured community banks increased by nearly 15 percent due to a jump in net interest income. Quarterly community bank net income increased by less than a half-percent to $8.3 billion due to increases in noninterest expenses and credit loss provisions. Pretax return on assets for community banks fell by two basis points from the third quarter to 1.49 percent.

Community banks reported a 3.7 percent increase in loan balances from the previous quarter and 14.4 percent increase from the fourth quarter of 2021. “Growth in nonfarm, nonresidential commercial real estate and one-to-four family residential mortgage loans drove both the quarterly and annual increase in loan balances,” the FDIC said.

The average community bank net interest margin increased 7 basis points from the third quarter and 48 basis points from the end of 2021 to 3.71 percent, which is higher than the pre-pandemic average of 3.63 percent.

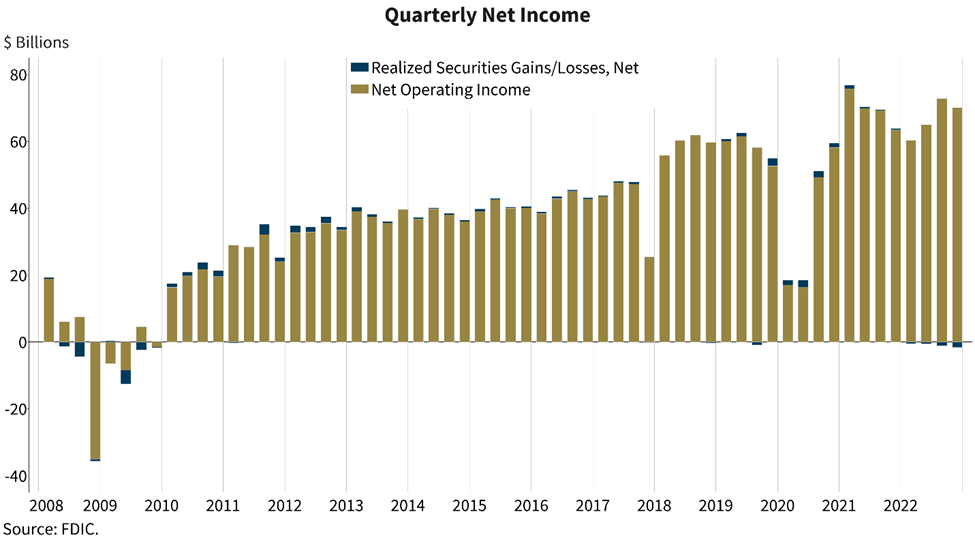

All FDIC-insured banks made $263 billion in net income last year, 6 percent lower than $279 billion in 2021. Banking income showed signs of recovering in the fourth quarter of last year: Year-over-year net income increased $4.5 billion (7 percent). Aggregate ROA fell to 1.12 percent last year from 1.23 percent in 2021. Overall NIM widened for the third straight quarter, increasing 23 basis points from the previous quarter and a record 82 basis points on an annual basis to 3.37 percent.

Total loan and lease balances increased by nearly 2 percent from the previous quarter. “The banking industry reported growth in several loan portfolios during the quarter, including consumer loans (Up $69.5 billion or 3.5 percent) and one-to-four family residential loans (up $43.8 billion, or 1.8 percent),” the FDIC said.

Other quarterly report findings included:

- Strong loan growth and higher market interest rates fueled a 76 basis point increase in the average yield on earning assets to 4.54 percent.

- Average funding costs increased 53 basis points from the prior quarter to 1.17 percent.

- Unrealized losses on securities fell 10 percent to $620.4 billion. Unrealized losses on held-to-maturity securities totaled nearly $341 billion, and unrealized losses on available-for-sale securities totaled $279.5 billion.

- Fueled by a rise in noncurrent credit card and C&I lending, loans 90 days or more past due increased one basis point to 0.73 percent. Total net charge-offs as a ratio of total loans increased 10 basis points from the previous quarter to 0.36 percent, which is still lower than the pre-pandemic average.

- According to the FDIC, 36 institutions merged in the fourth quarter, three de novo banks opened and no banks failed.

American Bankers Association Chief Economist Sayee Srinivasan said the report shows that the continued strength of the banking sector amid economic uncertainty.

“The banking industry remains well-capitalized and highly liquid,” he said. “That strength will help the nation’s banks weather potential headwinds as inflation and geopolitical risk persist.”