It’s hard not to be optimistic when someone drops some extra cash in your pocket, or when the people who wield power over you start to show some empathy.

The new year began in the wake of President Trump signing the 2017 Tax Cut and Jobs Act. Many banks responded by doling out tax bonuses to employees. “If this tax bill is going to have the impact that is being talked about, then you have to get it out there,” said Al Tubbs, chairman and CEO of Ohnward Bancshares, Maquoketa, Iowa. “You have to share it.”

The economy grew steadily throughout the year, though not as robustly as some had anticipated. Ernie Goss, economist at Creighton University in Omaha, said we were experiencing “a Goldilocks economy” as in “not too hot; not too cold.”

All that optimism from tax reform coupled with a “just right” economy was the perfect environment for a bipartisan, grassroots, all-hands-on-deck push for tiered regulation.

The darling bill of 2018 was, of course, S. 2155 (The Economic Growth, Regulatory Relief, and Consumer Protection Act), which garnered support in unexpected places. The Senate passed the bill during the Independent Community Bankers of America’s annual convention, but it took another two months for the House to figure out how to get the bill to the President without adding items that would cause Democratic support to vaporize.

The bill galvanized tiered regulation and elevated community banking as an industry clearly distinguishable in its needs and purposes from the nation’s largest banks — you know them, those nine institutions that hold half of the industry’s assets.

Later in the year, Karen Grandstrand would point to the passage of S. 2155 as predictive of increased industry consolidation, saying: “It increased the asset threshold for systemically important financial institutions to $100 billion from $50 billion immediately (and to $250 billion from $100 billion within 18 months) and reduces the number of banks subject to enhanced Fed supervision under Dodd-Frank rules to 22 from 38.” The M&A tide rolls on.

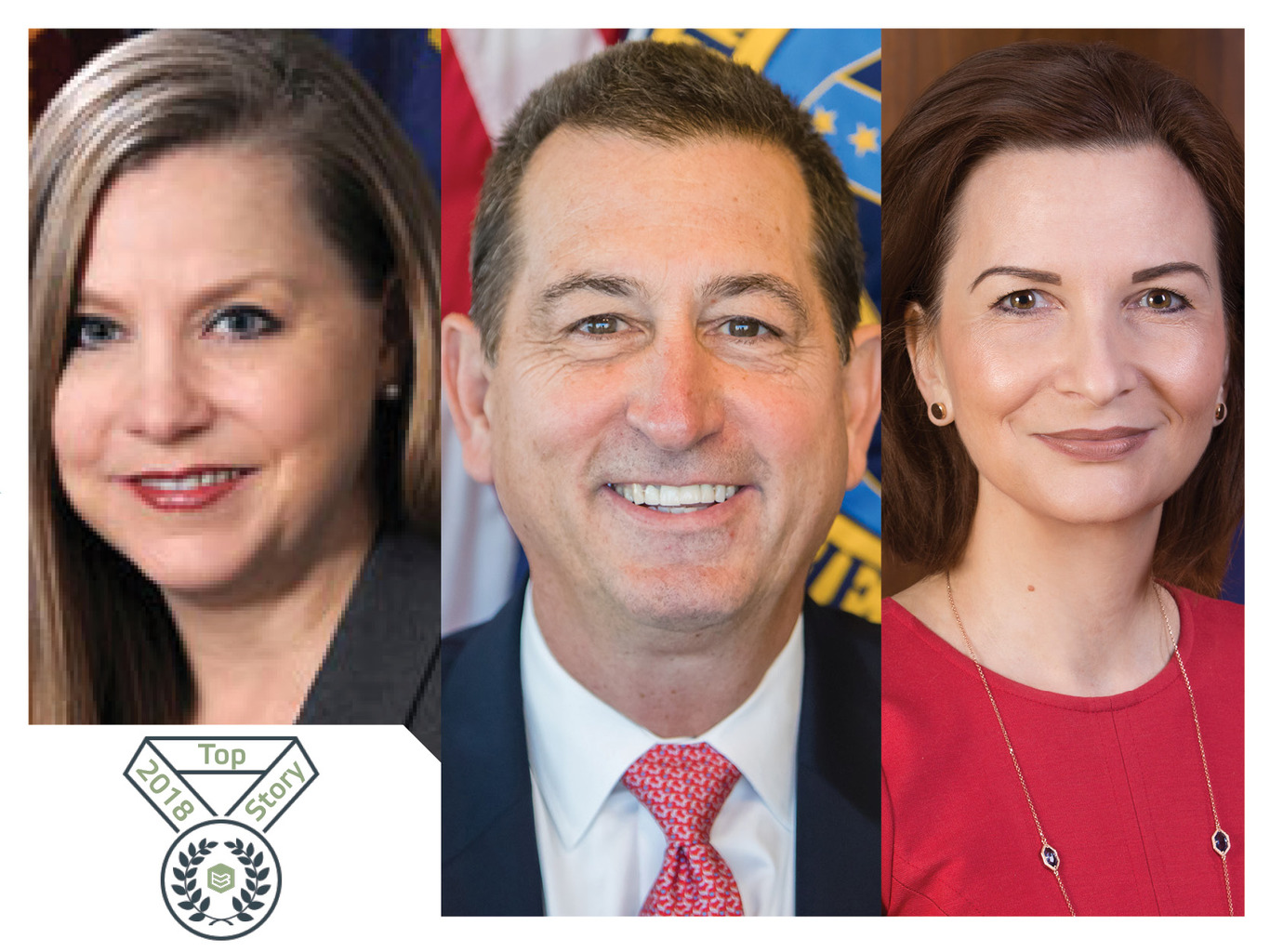

Just as significant a contributor to banker optimism as a partial roll-back of Dodd-Frank was the appointment of former bankers to lead the FDIC and the OCC. Richard Hunt, head of the Consumer Bankers Association, called the leaders of the regulatory agencies a “dream team.” Jelena McWilliams, chair of the FDIC, came out of Fifth Third Bank in Cincinnati while Joseph Otting, an Iowa native, worked at a handful of banks in California, including U.S. Bank. McWilliams has focused attention on minimizing the barriers of entry for new banks, while Otting has taken the lead on reforming the Community Reinvestment Act. Otting was also recently named acting director of the Federal Housing Finance Agency.

There has also been a change in leadership at the Consumer Financial Protection Bureau, with the confirmation just this month of Kathy Kraninger, who was nominated to head the CFPB (or whatever they are calling it these days) back in June.

Also in 2018, Michelle Bowman became the first person to fill the community bank seat on the Fed’s board. Bowman was former Kansas Banking Commissioner and is a fifth-generation community banker.