As the strategic planning process begins for 2021, bankers will reflect on the challenges and opportunities brought by the pandemic. With the transitioning political environment, continued vaccine development and rollout, and what looks to be a zero-rate environment for some time, 2021 will present different challenges — but opportunities as well. In particular, banks can plan to mitigate margin compression by aggressively lowering cost of funds, look for growth opportunities in what is expected to be an accelerating M&A environment, and consider other opportunities to build shareholder value as they meet the changing needs of their local communities.

Cost of funds in a zero rate environment must be evaluated carefully to find the balance, unique to each bank, of lower rates while maintaining the desired social image. Competitors such as online banks, fintechs and credit unions may seize the opportunity in this environment to offer substantially higher deposit rates but banks need to remain disciplined and consider their net interest margin. After all, loan rates will continue to fall to some floor so the same must be true for deposits. Effectively communicating the other services and benefits offered has always been a way to mitigate the loss of customers who are tempted by higher rates elsewhere. This is a delicate challenge that banks are accustomed to handling through various rate cycles and will need to do so again. Banks that are not able to manage their NIM could face shareholder pressure to improve profits or consider other alternatives such as a merger or outright sale.

Growth opportunities will exist in many markets as M&A returns to a more normal pace. This will be driven by underperforming banks whose shareholders don’t see imminent improvement in this low rate environment as well as banks who experience sector-specific asset quality weakness related to the new pandemic economy. Another source of growth through expansion will be the exodus of larger banks from some rural markets, opening the door for new branches or LPOs by community banks.

An ever-present condition supporting higher M&A volume is regulatory and political fatigue — with pending changes on the horizon in both areas, some management teams, director groups and shareholders may decide to seek an exit, particularly when succession issues exist.

After months of growth in the national debt and continued spending to support the economy, it’s difficult to see tax rates remaining unchanged for long. Rates at the corporate and personal level will affect C-corp and S-corp banks, another factor that will likely motivate merger activity as banks look to increased size, economies of scale, and cost savings to reduce pressure on profits. Changes in tax rates may also lead banks to evaluate the merits of their chosen tax structure versus need to access capital: As rates rise, more banks could convert to S-corp status if they feel their capital levels are not under pressure.

It would be incomplete to discuss M&A volume and pricing expectations without considering the market values of public bank stocks. On several occasions recently, news of effective vaccine trials provided a tremendous boost to stocks of banks. Historical research shows that the highest prices in bank M&A are paid by public banks using their stock as currency, and these price announcements trickle down to influence price expectations among smaller banks who may be selling for cash. The result: M&A pricing tends to ebb and flow with the change in public bank valuations. The low rate environment may prove difficult to overcome as public bank stocks seek to return to all-time highs set in 2018, but higher bank valuations are expected with an opening of the economy.

For more than a year, the phenomenon of banks issuing sub-debt has continued to gain favor as a way to benefit from the low rate environment. Whether refinancing existing debt or raising new funds for growth, sub-debt should continue to thrive as rates remain at historic lows. This presents an opportunity for banks to step into the other side of the trade by investing in the sub-debt being issued. This turns cash or low-yielding securities into what is a typically fixed-rate instrument for five years at 4 to 5 percent yield. While taxable, that’s likely to be a material improvement over the alternatives. Such an investment in the sub-debt of a handful of banks could provide meaningful yield and diversification to an investment portfolio.

A way to benefit from the currently depressed valuation environment is to consider stock buybacks. If a bank has shareholders in need of liquidity, a buyback program could make sense. Using excess capital or perhaps new funds from sources such as sub-debt to acquire one’s own stock could accomplish two objectives: Meet liquidity needs that may exist among a shareholder base, and build additional value over the long run for the shareholders who remain.

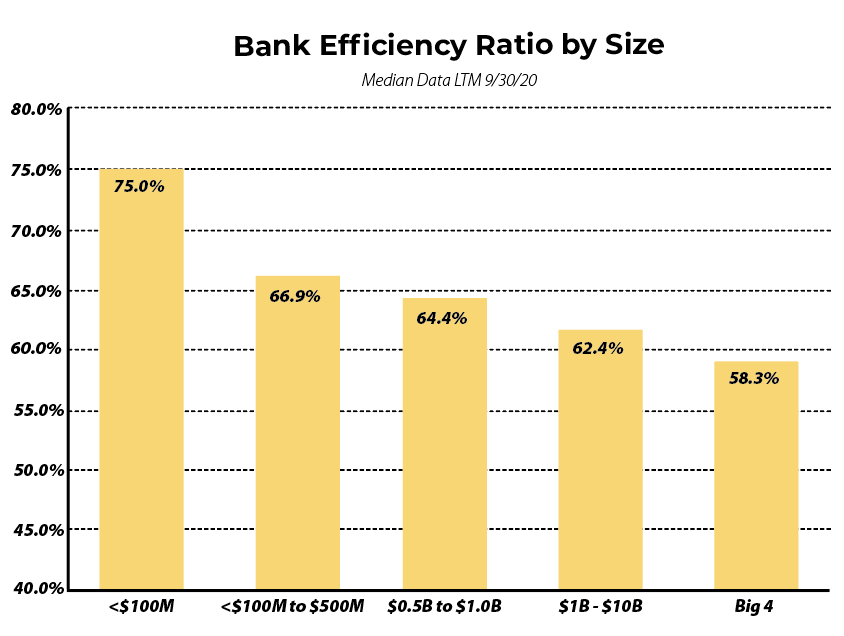

The inescapable truth as we anticipate banking in 2021: Asset size matters, as shown in the chart. While much of the macro banking, economic and interest rate environment is beyond the control of an individual bank, larger balance sheets are one of the few tools banks can control to overcome margin compression and other profit pressures. How to achieve growth, organically or through M&A, is unique to each bank but deserves careful consideration in strategic plans for 2021.

Amidst challenges new and old, the banking industry will continue to consolidate. As M&A accelerates and banks assess their long-term strategies post-pandemic, opportunities to build shareholder value will be identified, setting the course for management teams for the years ahead.

John Adams is principal and head of investment banking for Sheshunoff & Co., Dallas.