The Community Reinvestment Act is a federal law enacted in 1977 to encourage all depository institutions (excluding credit unions) to meet the credit needs of the communities in which they operate, including low- and moderate-income neighborhoods. The CRA was enacted in response to discriminatory lending practices known as “redlining,” where banks would deny loans to residents of certain areas based on racial or economic profiles. The legislation’s key aspects include:

- The CRA requires federal banking regulators (Federal Reserve, FDIC, OCC) to assess how well banks serve the credit needs of their entire communities, including low- and moderate-income areas.

- Regulators consider a bank’s CRA performance when evaluating applications for charters, branches, mergers and acquisitions.

- Banks are evaluated and rated on factors like lending, investments, and services in low-and moderate-income areas. Ratings range from “Outstanding” to “Substantial Noncompliance.”

- The CRA does not mandate specific lending requirements or quotas, but encourages banks to help meet community credit needs through safe and sound lending practices.

In essence, the CRA incentivizes banks to provide credit and banking services equitably across all neighborhoods they serve, including underserved areas, by tying regulatory approval to their CRA performance. For reference, the full list of CRA qualifying activities can be found here.

Previous attempts at modernization

Following the passing of the CRA legislation in 1977, the regulations officially took effect in 1978. Since then, U.S. banking regulators have made two sets of revisions, first in 1995 and again in 2005, with the most significant update in 1995. The need for revisions was born out of the fundamental shifts in the business of banking, and, more specifically, the changes in the way financial products and services are distributed — namely the reduced reliance on physical branch locations.

Most recent CRA update

The most recent update to CRA introduces several key changes to modernize and clarify the requirements. Notably, the update emphasizes a more nuanced approach to evaluating bank performance based on size and business model, and it introduces new data collection requirements to enhance transparency and accountability.

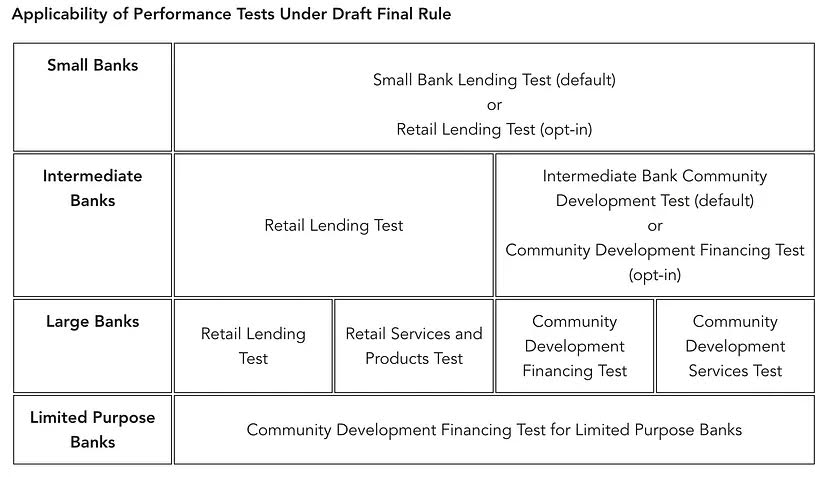

One significant change is the differentiation in requirements based on the size of financial institutions. Large banks now face more stringent reporting and assessment standards with new tests such as the retail services and products test, while the requirements for small banks have remained lesser and relatively consistent (the difference between large and small banks will be discussed in more detail in the next section).

Although the final rule is an interagency effort, its passage was not unanimous. The final rule had three votes against. Those individuals cited concerns over the final rule’s complexity, the agencies’ statutory authority, and whether its costs would outweigh the benefits.

Impact on community banks

The CRA’s requirements for community banks are tailored to balance their capacity and resources with their mission to serve their communities. Under the latest revisions, community banks must continue to demonstrate their commitment through small business lending, community development investments, and services that support local needs.

While the the term “community bank” typically refers to banks with less than $10 billion in assets, the CRA has historically made its own delineations based on asset-size thresholds. Those thresholds, which started at $250 million for small banks, have risen slowly over time to account for inflation. Currently, the thresholds are as follows:

- Small bank: less than $1.564 billion, as of Dec. 31 in either of the two prior years.

- Intermediate small banks: at least $391 million, as of Dec. 31 for both of the past two years; and less than $1.564 billion as of Dec. 31 in either of the two prior years.

- Large banks: at least $1.564 billion, as of Dec. 31 for both of the past two years.

Effective Jan. 1, 2026, the new thresholds will shift to:

- Small bank: less than $2 billion, as of Dec. 31 in either of two prior years.

- Intermediate small banks: at least $600 million, as of Dec. 31 for both of the past two years; and less than $2 billion as of Dec. 31 in either of the two prior years.

- Large banks: at least $2 billion, as of Dec. 31 for both of the past two years. While the threshold for large banks has increased to $2 billion, some critics of the legislation cite their disappointment with the lower than expected large bank threshold — noting the final rule does not go far enough to differentiate community banks from the large money center banks.

The full breakdown of CRA tests by bank type can be found below, according to Mayer Brown:

For community banks, staying compliant with the CRA can be both a challenge and an opportunity. Compliance requires a deep understanding of local needs and proactive engagement with community stakeholders. However, it also opens doors to strengthen relationships within the community, build trust, and ultimately drive local economic growth.

Leveraging technology for CRA compliance

Technology plays a key role in helping community banks navigate CRA compliance efficiently and effectively. Advanced data analytics and reporting tools enable banks to track and analyze their lending patterns, ensuring they meet regulatory requirements and identify areas for improvement. Moreover, digital platforms can facilitate greater community engagement, allowing banks to better understand and respond to the needs of their localities.

A few technology companies doing really great work that also help community banks meet their CRA requirements include:

- CNote, a BankTech Ventures portfolio company which offers corporations, institutions and individuals an effective way to invest in under-resourced communities. The company’s platform directs corporate cash into loan funds and insured deposit products at community financial institutions dedicated to economic equality, racial justice, gender equity and climate change.

- ColumnTax, which aims to democratize financial assistance by offering innovative tax solutions accessible to everyone. The company’s year-round, API-first tax products can be seamlessly and natively embedded to ensure community banks continue to serve their customers in meaningful ways.

- Payitoff, which is a debt infrastructure company that helps financial institutions save borrowers an average of $240 per month on federal student loans. The company’s tools automate guidance, enroll borrowers in cost-saving repayment options, and integrate student loan workflows with ease.

- Ned, which is an end-to-end cash flow underwriting and servicing system enabling community banks to provide a range of revenue-based financial products while streamlining qualification, disbursement and repayments. Ned’s platform helps lenders qualify more borrowers at cost, specifically those in lower-to-moderate income neighborhoods.

Conclusion

CRA remains a cornerstone of equitable banking, continuously evolving to address new challenges and opportunities. The requirements of the final rule will be phased in periodically through Jan. 1, 2026. For community banks, understanding the historical context, staying abreast of recent updates, and leveraging technology are critical steps toward meaningful compliance.

By doing so, they not only fulfill regulatory obligations but also strengthen their role as vital engines of local economic development. For more information on the specifics of each test, their corresponding weights by bank type, and the phased rollout of requirements, you can reference this great resource published by Mayer Brown.

Jake Fuchs works on the BankTech Ventures investment team, based out of New York City. Fuchs previously helped launch Primetime Partners, a $50 million venture fund that invests in products, services, and experiences that cater to the older adult demographic.