Net income at FDIC-insured community banks fell nearly 5 percent to $6.7 billion during the third quarter, according to the agency’s Quarterly Banking Profile.

Net income at FDIC-insured community banks fell nearly 5 percent to $6.7 billion during the third quarter, according to the agency’s Quarterly Banking Profile.

The income drop was caused by a rise in losses on the sales of securities and higher noninterest expenses which more than offset higher noninterest income, according to the Nov. 29 report. Net income fell 15 percent or $1.2 billion from the third quarter of 2022 due to higher noninterest expenses and lower net interest income. Total community bank deposits fell for the sixth straight quarter as asset quality metrics remained positive despite some deterioration.

Community banks reported a 1.7 percent rise in loan balances from the second quarter and a nearly 10 percent increase on an annualized basis. The increases were attributed to growth in one-to-four family residential mortgages and nonresidential, nonfarm commercial real estate loans.

Community banks’ NIM fell for the third consecutive quarter, this time down four basis points to 3.35 percent, which is 28 basis points lower than the third quarter of 2022. The yield on earning assets increased 21 basis points on a quarterly basis, while the cost of funds rose 25 basis points on a quarterly basis.

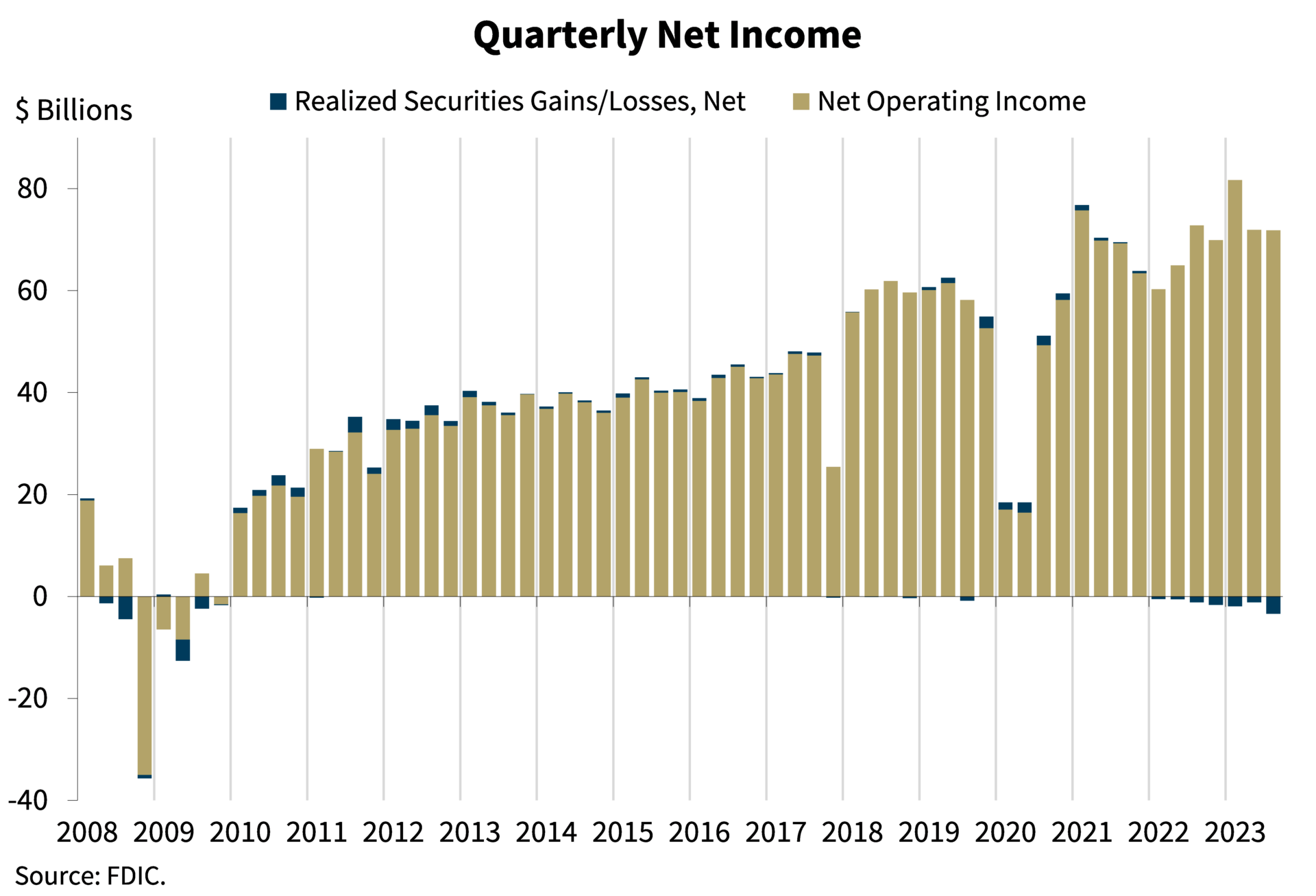

The nation’s 4,614 FDIC-insured commercial banks and savings institutions reported $68.4 billion in net income in the third quarter, down 3.4 percent or $2.4 billion from the second quarter. The decrease was attributed to a 5.2 percent fall in noninterest income and $3 billion rise in realized securities losses.

First and second quarter bank income benefited from gains from the accounting treatment for the acquisitions of failed banks Silicon Valley Bank, Signature Bank and First Republic Bank. According to the FDIC, net income excluding those one-time gains would have been flat for the past four quarters.

FDIC-insured banks reported a 1.17 percent average return on assets in the third quarter, down from 1.21 percent the previous quarter. NIM increased three basis points to 3.30 percent, above the pre-pandemic average of 3.25 percent as deposit expenses increased faster than loan yields.

Nearly $684 billion in unrealized securities losses were reported in the third quarter, up 22.5 percent or $125.5 billion. Loan and lease balances increased 0.4 percent from the second quarter to $45.9 billion amid an increase in credit card loans and one-to-four family residential mortgages.

Loan performance numbers remained positive. Sparked by nonfarm, nonresidential CRE loan balances, loans 90 days or more past due increased seven basis points to 0.82 percent, which is still well below the industry’s 1.28 percent pre-pandemic average. Net charge-offs as a ratio of total loans increased two basis points from the previous quarter and 25 basis points from the prior year to 0.51 percent, which also remains below its pre-pandemic average.

“The banking industry continued to show resilience in the third quarter,” said FDIC Chair Martin Gruenberg. “Net income remained high, overall asset quality metrics remained favorable, and the industry remained well capitalized. The banking industry still faces significant downside risks from the continued effects of inflation, rising market interest rates and geopolitical uncertainty.”

Other 3Q report findings included:

- Deposits fell for the sixth straight quarter, down a half percent to $90.4 billion.

- The Reserve Ratio for the Deposit Insurance Fund increased two basis points to 1.13 percent. Sparked by increased assessment revenue, the Deposit Insurance Fund balance increased approximately $2.4 billion to $119.3 billion.

- Two banks opened in the third quarter, while 28 merged and two voluntarily liquidated.