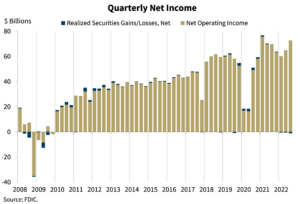

FDIC-insured institutions made $71.7 billion in the third quarter, an 11.3 percent increase from the previous quarter.

The increase, reported Dec. 1 as part of the FDIC’s Quarterly Bank Profile, was sparked by a rise in net interest income, which more than offset a rise in provisions for credit losses, according to the FDIC. Year-over-year net income increased by $2.2 billion (3.2 percent). Nearly three quarters of banks experienced an increase in net income from the previous quarter.

Net interest margins increased by a record 35 basis points from the second quarter and 58 basis points from the third quarter of 2021 to 3.14 percent. NIM, which is above 3 percent for the first time since the first quarter of 2020, remains below its pre-pandemic average of 3.25 percent.

Community bank quarterly net income increased by $1 billion (13.5 percent) from the previous quarter to $8.5 billion. Net income was up by $317 million (nearly 4 percent) from a year ago.

Community bank loan balances increased by 4.1 percent from the previous quarter and 12.2 percent on an annual basis. “Growth in commercial real estate and one-to-four family residential mortgage loans drove the quarterly increase in loan balances for community banks, while growth in commercial real estate loans drove the annual increase,” the FDIC stated. percent. Net interest income for community banks increased 30 basis points from the previous quarter and 32 basis points from a year ago to 3.63 percent. The average yield on earning assets increased 48 basis points on a quarterly basis.

Loan and lease balances for all banks increased by 2 percent ($229 billion) from the previous quarter. Several loan portfolios grew during the third quarter, including one-to-four family residential loans by nearly 3 percent and consumer loans by 2 percent. Year-over-year loan and lease balances grew by nearly 10 percent ($1.1 trillion), a record increase sparked by increases in commercial and industrial loans, family residential mortgages and consumer loans. The percentage of noncurrent loans dropped 3 basis points from the previous quarter to 0.72 percent, its lowest percentage in 16 years.

FDIC Acting Chair Martin Gruenberg said additional interest rate hikes from Federal Reserve Open Market Committee along with longer asset maturity spans could pose problems for banks in the coming quarters.

“Despite several favorable performance metrics in the third quarter, the banking industry continues to face significant downside risks,” he said. “These risks include the effects of inflation, rising market interest rates, and continued geopolitical uncertainty. Taken together, these risks may reduce profitability, weaken credit quality and capital, and limit loan growth in coming quarters.”

Other report findings included:

- Unrealized losses on available-for-sale and held-to-maturity securities increased 47 percent ($690 billion) from the previous quarter.

- Strong loan growth and rising interest rates caused the average yield on earning asset yields to increase by 73 basis points from the previous quarter to 3.78 percent. Average funding costs increased 38 basis points to 0.64 percent.

- The aggregate return on average assets ratio was at 1.21 percent, a 13 basis point increase from the second quarter but unchanged from the previous year.

- The reserve ratio for the Deposit Insurance Fund remained at 1.26 percent.

- Three new banks opened, including Walden Mutual Bank, Concord, N.H.; GS&L Municipal Bank, Gouverneur, N.Y.; and Bank Irvine, Irvine, Calif.