FDIC-insured community banks made $5.9 billion in net income during the fourth quarter of last year, down 9.9 percent or $650.2 million from the previous quarter. The drop was caused by higher noninterest and provision expenses, according to the FDIC’s Quarterly Banking Profile.

FDIC-insured community banks made $5.9 billion in net income during the fourth quarter of last year, down 9.9 percent or $650.2 million from the previous quarter. The drop was caused by higher noninterest and provision expenses, according to the FDIC’s Quarterly Banking Profile.

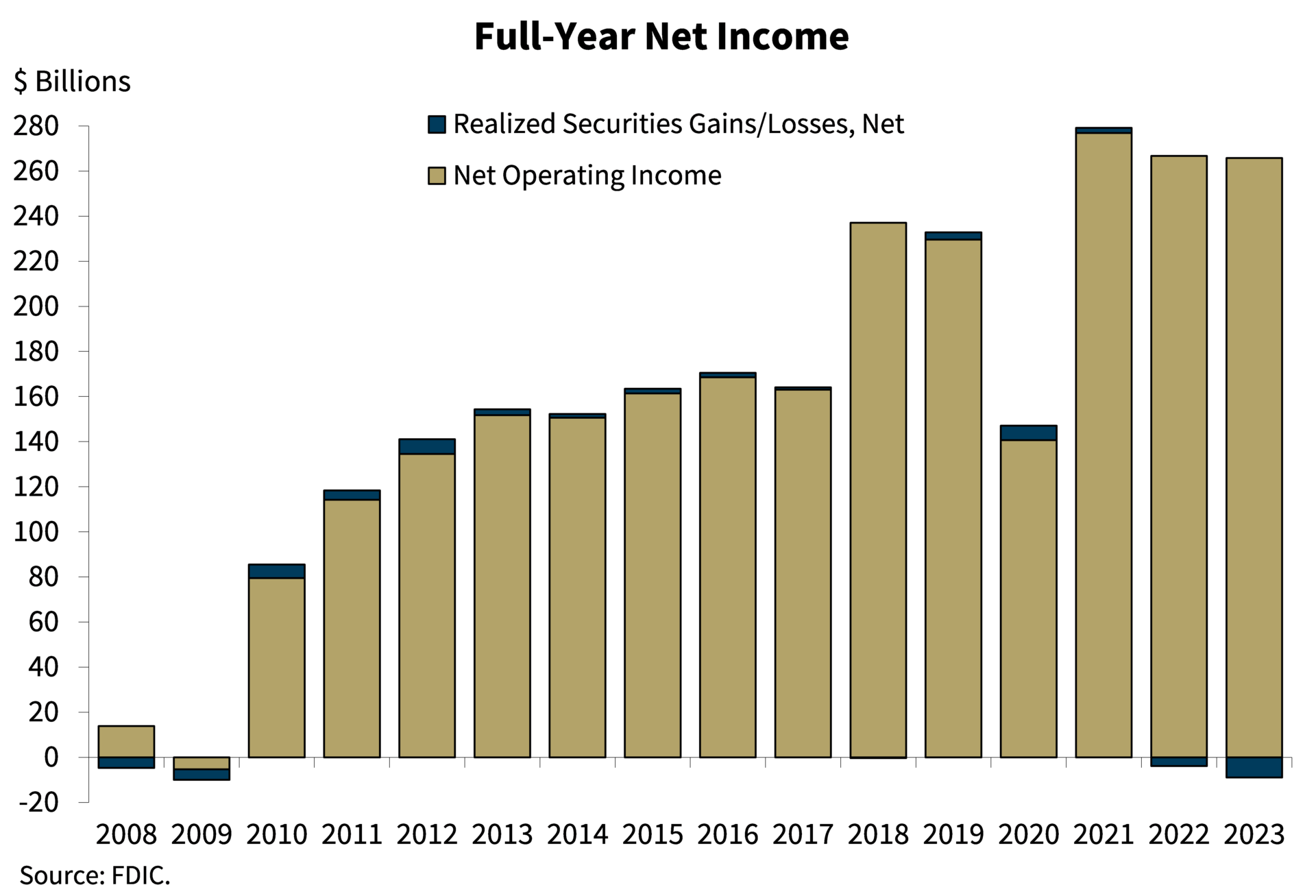

Community banks reported $26.6 billion in net income in 2023, down 7.1 percent or $2 billion from the previous year, as higher noninterest and provision costs offset a rise in net operating revenue.

Community bank loan balances increased 1.8 percent from the third quarter of 2023 and 7.8 percent from the previous year. “Community bank loan growth has been broad-based, with quarterly and annual increases reported across all major loan categories,” according to the March 7 report. “The growth has been strongest in residential mortgage loan balances and nonfarm, nonresidential commercial real estate loan balances.”

Community banks reported a full-year, pre-tax return on assets of 1.22 percent last year, down 17 basis points from 2022. Community banks’ pretax ROA in the fourth quarter fell 15 basis points from the previous quarter to 1.07 percent. Community banks’ NIM was 3.35 percent, unchanged from the third quarter but 28 basis points lower than its pre-pandemic average.

FDIC-insured commercial banks and savings institutions made $38.4 billion in net income in the fourth quarter of last year, down nearly 44 percent or $30 billion amid a 19 percent rise in noninterest expenses and 26.5 percent increase in provision expenses.

“However, it is estimated that 70 percent of the decrease in net income was caused by specific, nonrecurring, noninterest expenses at large banks,” according to the FDIC. “These expenses include the special assessment, goodwill impairment, and legal, reorganization and other one-time costs.”

Banks made $256.9 billion in net income last year, down 2.3 percent or $6 billion from 2022 as higher noninterest and provision expenses along with realized losses on securities counteracted net operating revenue growth. Banks’ aggregate ROA fell one basis point to 1.10 percent.

Net operating revenue rose from the previous quarter amid a rise in net interest income. Sparked by a 6 percent rise in credit card lending, total loan and lease balances increased nearly 1 percent from the third quarter to $107.5 billion, the industry’s highest loan growth rate reported last year.

Total loan and lease balances rose nearly 2 percent or $225.1 billion in 2023 amid increases in credit card loans and one-to-four family residential loans. More than 85 percent of banks experienced annual loan growth last year.

Unrealized securities losses fell 30 percent to $477.6 billion in the fourth quarter of last year — its lowest mark in nearly two years — amid a drop in unrealized losses on residential mortgage-backed securities.

Banks’ NIM fell two basis points from the third quarter to 3.28 percent as the rise in deposit and non-deposit liability expenses outpaced an increase in asset yields. Domestic deposits rose 1.1 percent, its first increase in nearly two years, amid a growth in time deposits. The noncurrent loan rate increased but remained under pre-pandemic averages.

FDIC Chair Martin Gruenberg said the industry “has shown resilience after a period of liquidity stress in early 2023. Full-year net income remained high, overall asset quality metrics were favorable, and the industry’s liquidity was stable. However, ongoing economic and geopolitical uncertainty, continuing inflationary pressures, volatility in market interest rates, and emerging risks in some bank CRE portfolios pose significant downside risks to the banking industry. These issues, together with funding and earnings pressures, will remain matters of ongoing supervisory attention by the FDIC.”

Other report findings included:

- Delinquency rates increased in the fourth quarter, mainly due to credit cards, but continued to be under pre-pandemic averages. Loans 90 days or more past due or in nonaccrual status increased four basis points to 0.86 percent of total loans. The share of loans 30-89 days past due increased seven basis points to 0.61 percent.

- Sparked by credit card chargeoffs, the net chargeoff rate increased 14 basis points from the third quarter to 0.65 percent. The net chargeoff rate at community banks was 0.18 percent.

- The deposit insurance fund reserve ratio increased to 1.15 percent. Sparked by a rise in assessment revenue, the DIF balance increased $2.4 billion to $121.8 billion.

- The number of FDIC-insured institutions fell by 27 in the fourth quarter to 4,587. Twenty-three institutions merged with other banks. One bank opened, while one bank failed.