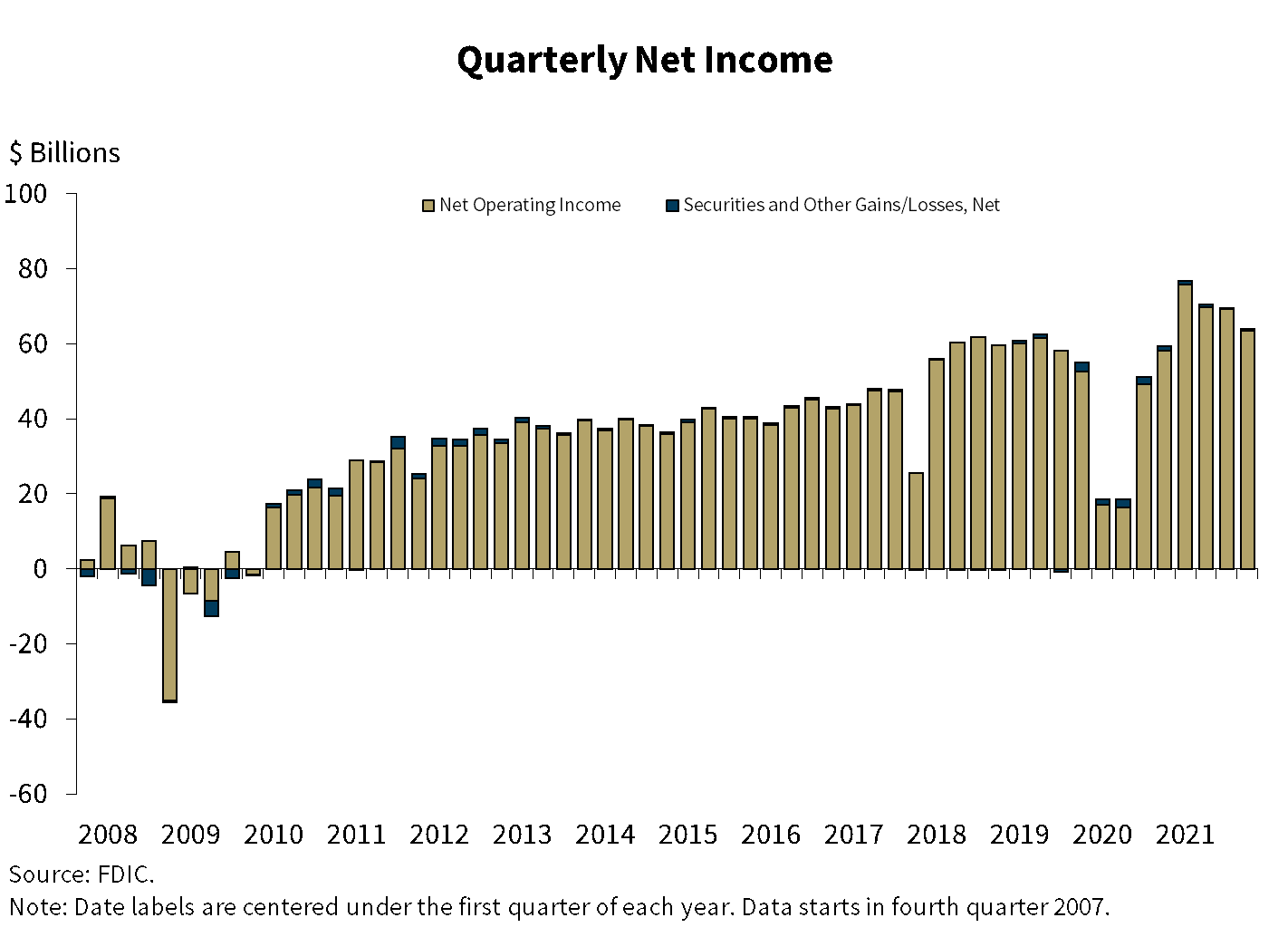

Banks and savings institutions insured by the Federal Deposit Insurance Corporation made $63.9 billion in net income during the fourth quarter of 2021, according to the latest Quarterly Banking Profile. That’s down slightly from the previous quarter’s $69.5 billion in net income.

Banks and savings institutions insured by the Federal Deposit Insurance Corporation made $63.9 billion in net income during the fourth quarter of 2021, according to the latest Quarterly Banking Profile. That’s down slightly from the previous quarter’s $69.5 billion in net income.

The $4.4 billion, 7.4 percent year-over-year increase was driven by ongoing economic growth and improved credit conditions, according to the FDIC, which led to a $5.8 billion increase in bank net interest income and $4 billion decline in provision expenses.

Based on those same factors, community banks’ year-over-year net income grew $511.6 million in the fourth quarter. Net interest income for community banks, however, declined less than 1 percent or $165.8 million from the previous quarter. Year-over-year provision expenses declined by 74 percent or nearly $915 million but increased nearly 14 percent or $39.2 million from the previous quarter. Community banks’ year-over-year net interest margin narrowed 11 basis points to 3.22 percent as earning assets growth outpaced increases in net interest income. More than half of the 4,391 FDIC-insured community banks reported higher quarterly net income. Sparked by a growth in nonfarm, nonresidential CRE loan balances, community banks’ loan balances increased 1.4 percent from the previous quarter and 2 percent from 2020.

The banking industry as a whole had nearly $280 billion in net income last year, an 89.7 percent increase from $132 billion in 2020. The average ROA increased from 0.72 percent in 2020 to 1.23 percent last year.

“The FDIC’s latest quarterly report on the health of America’s banks shows that the industry ended the year on firm footing as the economy continued its return to normalcy. Deposit growth remained strong while credit availability and demand continued on their promising upward trajectory,” said Sayee Srinivasan, chief economist and head of research at the American Bankers Association.

Loan balances increased $326 billion or 3 percent from the previous quarter. This growth was driven by many portfolios expanding, including consumer loans by $84.9 billion or 4.7 percent; commercial and industrial loans by $70.8 billion or 3.2 percent; and loans to nondepository institutions by $59 billion or 9.1 percent. Total loan and lease balances increased $383.2 billion or 3.5 percent on an annual basis. This growth was also driven by the expansion of many portfolios, including consumer loans by $137.8 billion or 7.9 percent; loans to nondepository institutions up $124.5 billion or 21.5 percent; and nonfarm, nonresidential CRE loan balances up $77 billion or 4.9 percent. These increases helped offset a 5.2 percent drop in C&I loans caused by Paycheck Protection Program loan forgiveness and repayment.

“Total lending saw healthy growth and momentum over the quarter,” Srinivasan said. “Consumer lending was particularly strong and small business lending showed encouraging growth.”

Credit quality continued to improve in the fourth quarter: Outstanding loan balances at least 90 days overdue continued to decline, down $3.1 billion or 3 percent from the previous quarter. The noncurrent rate for total loans dropped five basis points from the previous quarter to 0.89 percent. The net charge-off balance continued its ongoing decline, down $5.6 billion or 49.5 percent from a year ago. The total net charge-off rate fell 21 basis points to 0.21 percent, near the third quarter’s record low.

A slight majority of banks reported annual improvements in quarterly net income, but net income still fell 8.1 percent from the third quarter, mainly due to a quarter-to-quarter increase in provision expenses.

Industry-wide, NIM remained low. The margin didn’t change from the third quarter at 2.56 percent, six basis points higher than the record low during the second quarter of 2021 but still down 12 basis points from the previous year. The yield on earning assets slightly declined to 2.71 percent, down two basis points from the previous quarter and 21 basis points year-over-year. Average funding costs dropped two basis points from the third quarter to a record low of 0.15 percent.

According to the FDIC, 72 institutions merged and no banks failed in the fourth quarter. For the first time in three years, no bank failures were reported in 2021.